Detailed accounting model

|

Detailed accounting model |

|

|

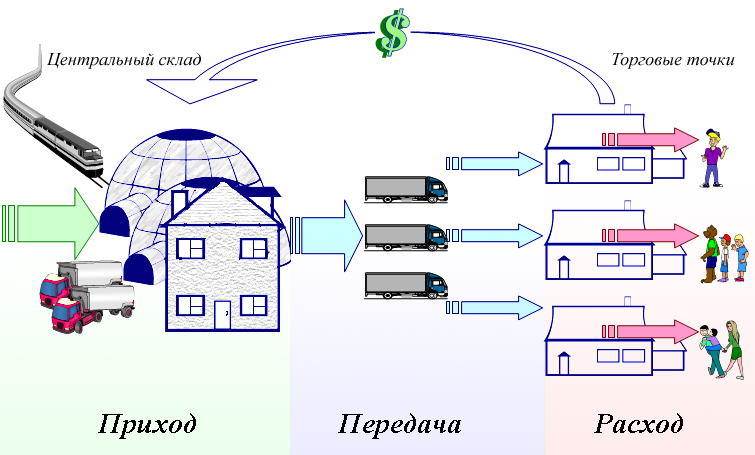

We assume that the system has a few outlets. For each point monitored ward, consumption, transfer of goods between two points, is cash. This is a detailed model of accounting. The result is a full real picture of the entire trade and warehousing system.

Most of the arrival of the goods carried to the central warehouse from which with the help of overhead on the transfer of goods are distributed on the points. Since the terms of the program, all points are equal, such a model the movement of goods is not mandatory. However, for organizational reasons, it is convenient to select one of the points as the home or center. This model is ideal for companies with several closely-spaced outlets. If the firm is engaged in wholesale trade, it is assumed that the release of goods is carried out with an extract of overhead expense, which is easy to transmit regularly to the firm for the wiring through the system. Thus, even if the outlets geographically remote, it is easy to arrange delivery of invoices (or copies thereof) at the firm to continuously monitor the residues at a remote point. At any time you can get a statement of balances, go to the point and produce a reconciliation. The main difficulties faced by the user, there are, if its outlets intensive retail and is the inability to provide operational data on these points. Suppose the point sell goods and sell in an intensive mode (as an example - a grocery store during rush hour). Of course, of no account in real time, not a speech. Accounting begins when the inventory begins. Point of sale inventory produces and directs us to rediscount bill, which is essentially a statement of balances at the time of stocktaking. In this case, already does not matter how often the inventory is carried out - every night once a week or once a month. The important thing - we do not see the real picture of the outlet in between rediscount. The picture will be even more distorted, the more time intervals of rediscount to rediscount. If a large range of products (more than 600-700 items), and the inventory are made is rare, raises a reasonable question - how important for us to keep track of balances, which are already reflected a long delay, given that labor costs for recordkeeping for remote sales outlets are significant ? My head pops the famous phrase - "accounting and control." Accounting in this case, it turns out "so-so", but the control turns "is even nothing." What is the control. When we are given statement for re-registration, it is usually signed, that is the team that conducted the inventory assures its correctness, and in case of problems, is responsible. Rediscount bill contains, as a rule, the name of the product, its quantity, retail price, sometimes the purchase price, up to the line. At the end of the report calculated the total amount of goods at retail prices. Besides the remote point of sale proceeds rents for a certain amount, which necessarily must be equal to the amount sold. It is obvious that the amount of goods sold will be equal to

Sper Spr=n-1 + Spost - Sper n,

where Spr - sum of goods sold, Sper n-1 - the total amount of goods at retail prices of the previous re-registration, Sper n - the total amount of goods at retail prices on the current re-registration, Spost - the amount transferred from the central warehouse of goods at retail prices. Simply put, how much money of goods sold, so revenue must pass. Common ploy in the preparation of rediscount statements is a distortion of the final amount in the desired direction (usually a big one. That is really at the point of goods is lower in the outcome of a large amount of writing that the amount of revenue converged). In this case, control is performed when entering the expenditure bill. Remains of goods from the rediscount statements carried in the field of new balances expenditure bill, as a result of the amount consumed will be calculated automatically as the difference existing in the program number and a new number for re-registration. The system itself podobet total expenditure on consignment, as a result of the amount of consumable goods in retail prices should be equal to the amount provided by revenues. In case of discrepancies are investigated, to find and fix the cause. Another type of error that the program allows you to fish, is to track changes in the balances of the warehouse. Knowing the amount of goods on the previous re-registration, the number of the same product that has been transferred from the warehouse and the quantity of goods on the current re-registration, it is easy to see pattern, which can be expressed as the inequality

Kper n <= Kper n-1 + Kpost,

where Kper n - number of the product on the current re-registration, Kper n-1 - the number of the same product on the previous re-registration, Kpost - the number of goods transferred from the central warehouse. In other words, the product of the new re-registration can not be larger than the previous re-registration in the light transmitted from the central warehouse number. If the goods on a new re-registration was more to look for any error in the results of the last stocktaking or as a result of this. |